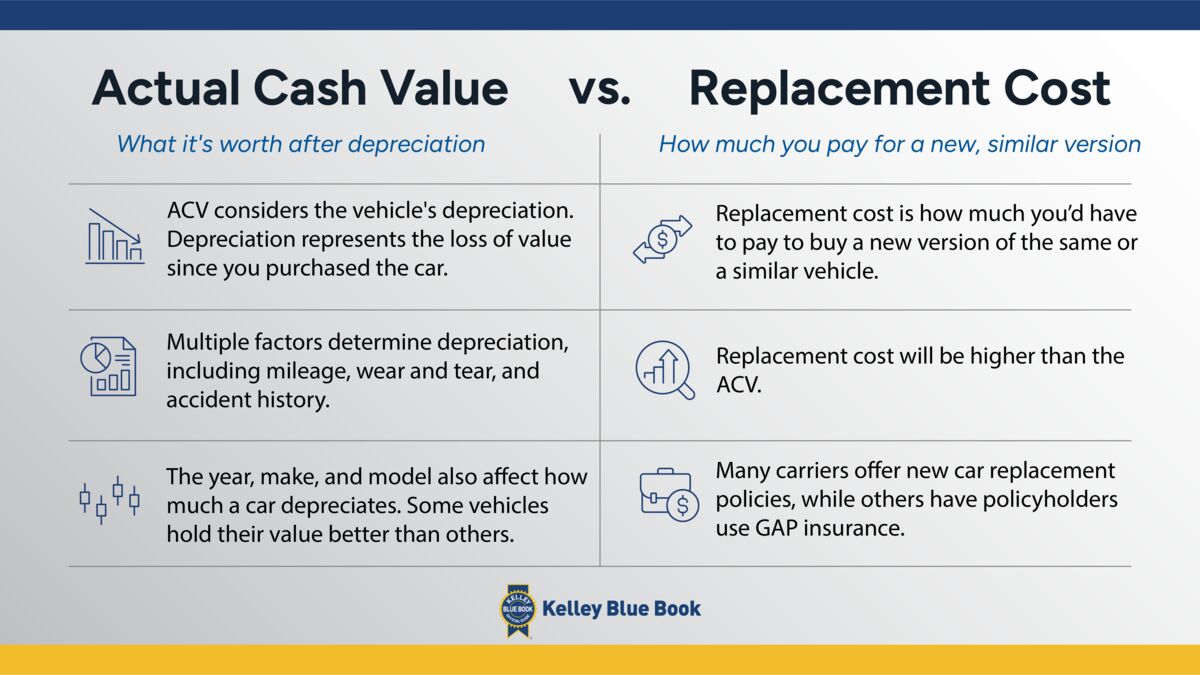

Because cars depreciate so quickly, it’s easy to become upside down on an auto loan or lease, especially if you put little or no money down. GAP insurance coverage, or guaranteed asset protection, can help mitigate this risk. It helps pay the difference between what your car is worth and what you owe the lender or leasing company. Some car lease contracts require GAP coverage.

Many GAP policies even cover your collision or comprehensive deductible. And with GAP coverage, you won’t have to worry about whether the ACV of your vehicle is high enough to pay off your loan or lease. Many drivers carry GAP insurance during the first several years of owning a car.

For example, if you owe $40,000 on your car loan, wreck the car, and your vehicle’s actual cash value is $33,000, your insurance company will pay $33,000. You’ll have to come up with the extra $7,000 to pay off your loan. But GAP insurance, if you have it, covers the additional $7,000 for the replacement value. In this case, being covered for replacement value with GAP insurance makes sense.

For car buyers who pay cash outright when they purchase a vehicle, it doesn’t make sense to carry GAP insurance because they don’t have any loan differences to worry about.